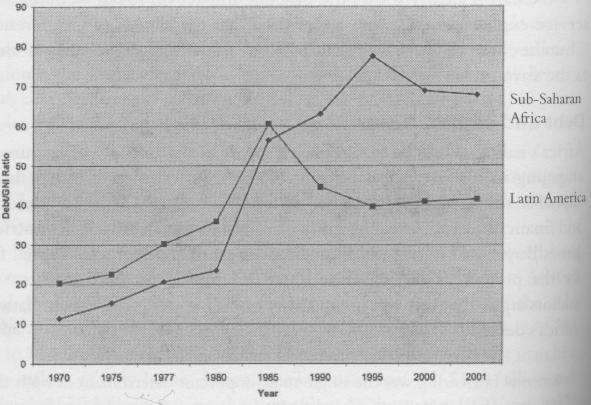

Chart 1: Debt Burdens of Sub-Saharan Africa and Latin America,

1970–2001

Source: World Bank, Global Development Finance Tables

ISJ 2 Index | Main Newspaper Index

Encyclopedia of Trotskyism | Marxists’ Internet Archive

From International Socialism 2 : 107, Summer 2005.

Copyright © International Socialism.

Copied with thanks from the International Socialism Website.

Marked up by Einde O’Callaghan for ETOL.

Gordon Brown has trumpeted loudest about his initiatives to reduce

Africa’s debt. If we are to believe the newspaper headlines and

even the hype of some NGOs, the chancellor has not only led the way

in tackling the debt of the world’s poorest countries, but is now

proposing to wipe it out altogether. All of this is a pack of lies.

But Brown and his cheerleaders are able to get away with it because

the issues around the debt are usually presented as too complex for

ordinary people to grasp. Once we penetrate behind the deliberately

mystifying terminology, however, the immense scandal of the debt and

Brown’s part in perpetuating is clear for all to see.

The first feature of the African debt is the remarkable extent to which it has contributed to the continent’s immiseration. Its size does not appear particularly onerous at first sight. In 2003 the total external debt of sub-Saharan Africa stood at $213.4 billion, as compared to Brazil’s $235.4 billion, the total for Latin America and the Caribbean of $779.6 billion, and of the South as a whole of $2,500 billion – a record high. [1] Meanwhile, the accumulated debt of the world’s richest country, the US, had reached $2,300 billion. [2] Against this backdrop of rising global indebtedness, daily foreign exchange transactions accelerated from $800 billion in 1992, to $1.2 trillion in 1995 and nearly $1.6 trillion in 1998. [3] Africa’s debt is thus a tiny drop in the ocean of international finance.

But African debt has distinctive features which have arguably made it the worst in the Third World. The debt is massive compared to the size and repayment capacity of the African economies sucking a proportionally greater volume of scarce resources out and directly impoverishing the region. Already marginal to the global system, sub-Saharan Africa plummeted faster and further than any other Third World region since the debt crisis of the early 1980s struck. By 1987 only 12 out of 44 African countries were able to regularly service their debts without debt relief. [4] The remainder were locked into an infernal cycle of further borrowing, compounding interest and accumulating debt stock and arrears [see Table 1]. A good indicator of a country or region’s real debt burden is the relationship between the size of its debt and the size of its economy as indicated by gross national income (GNI) or gross national product (GNP). The true picture of Africa’s multiplying debt burden was captured by the American NGO Africa Action in 2001:

bq. The ratios of foreign debt to the continent’s gross national product (GNP) rose from 51 percent in 1982 to 100 percent in 1992, and its debt grew to four times its export income in the early 1990s. In 1998, sub-Saharan Africa’s debt stock was estimated at $236 billion, and that of the whole continent was over $300 billion. Africa’s debt burden is twice that of any other region in the world – it carries 11 percent of the developing countries’ debt, with only 5 percent of its income. GNP in sub-Saharan Africa is $308 per capita, while its external debt stands at $355 per capita. [5]

|

Table 1: Sub-Saharan Africa's External Debt, 1970–2002 |

||||||

|---|---|---|---|---|---|---|

|

|

1970–79 |

1980–89 |

1990–99 |

1990–96 |

1997–99 |

2000–02 |

|

Total Debt |

21,859 |

104,676 |

208,436 |

202,821 |

221,536 |

208,334 |

|

Arrears |

602 |

5,988 |

33,539 |

30,743 |

40,064 |

25,600 |

|

Debt service paid |

1,667 |

8,823 |

12,415 |

11,463 |

14,637 |

12,872 |

|

Total debt/ |

66.0 |

159.0 |

237.5 |

243.2 |

226.3 |

184.2 |

|

Debt service paid/ |

5.0 |

13.4 |

14.1 |

13.7 |

15.0 |

11.4 |

|

Source: UNCTAD, Debt Sustainability: Oasis or Mirage? (2004), p. 6 |

||||||

|

Chart 1: Debt Burdens of Sub-Saharan Africa and Latin America, |

|---|

|

|

|

Source: World Bank, Global Development Finance Tables |

As Chart 1 shows, Africa’s debt–GNI ratio had not only overtaken that of Latin America by the 1980s, but continued to sharply rise through the 1990s while Latin America’s fell.

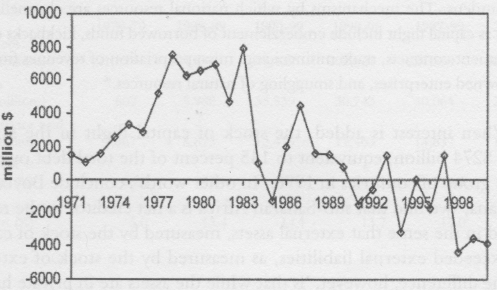

The huge increase in Africa’s debt burden was accompanied by a massive outflow of resources to foreign creditors. sub-Saharan Africa’s annual debt service payments – i.e. the money spent paying back the debt and the interest on it – expanded from an average of $1.7 billion in 1970–1979 to $14.6 billion in 1997–1999. [6] The huge outflows were not matched by the inflow of new loans. Africa received total loans of $540 billion and paid back $550 billion during the three decades between 1970 and 2002, while retaining a total debt of $295 billion [7] [see Chart 2]. In 1990 African countries paid out $60 billion more than they received in new loans and by 1997 this had increased to £162 billion. [8] The 1990s were a period of worsening resource transfers – a trend which continued into the new millennium. In 2001 sub-Saharan Africa borrowed $11.4 billion, but paid back $14.5 billion – a net transfer of $3.1 billion. [9]

The social and economic cost of servicing Africa’s debt has been immense. Year on year greater proportions of shrinking national budgets were diverted to repaying Western creditors at the expense of welfare or productive investment. During the 1980s debt service payments averaged 16 percent of African government expenditure compared to 12 percent on education, 10 percent on defence and 4 percent on health. [10]

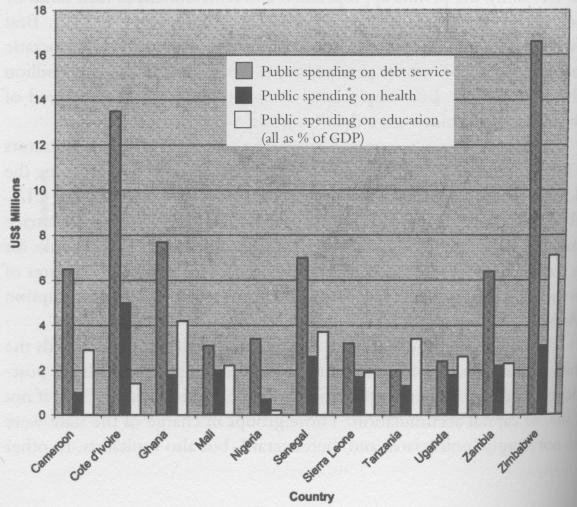

The prioritisation of interest payments over human need was no less appalling a decade on. In 1999 creditor pressure forced the Zambian government to spend $14 million more in debt service than on its collapsing healthcare system as the AIDS pandemic reached new heights. [11] The same year 33 percent of Angola’s GDP was sucked into debt repayments compared to 4.9 percent and 1.4 percent of GNP invested in education and health. [12] In 2001 debt service in sub-Saharan Africa as a whole amounted to 3.8 percent of GDP, compared to the 2.4 percent of GDP spent on health. [13]

Chart 3 clearly shows the obscene impact on social welfare of debt service expenditure. Little wonder then that the all-Africa Conference of Churches has called Africa’s debt burden ‘a new form of slavery, as vicious as the slave trade’. [14]

|

Chart 2: The Worsening Resource Transfers of |

|---|

|

|

Source: J. Boyce & L. Ndikumana, Africa’s Debt: Who Owes Whom?, |

|

Chart 3: The Differences Between Public Expenditure on Debt Service |

|---|

|

|

Source: K. Osuwu et al., Through the Eye of a Needle (Jubilee 2000 Coalition, 2000) |

Africa’s ruling classes have also played a part in the outflow of resources by engaging in massive ‘capital flight’. This is the transfer of locally owned capital to the advanced economies where it is typically invested in property and financial assets. A recent study of 30 sub-Saharan African countries by James Boyce and Leonce Ndikumana has estimated that total capital flight for the period 1970–1996 stood at $187 billion in 1996 dollars. [15] The authors argue that this was inextricably bound up with the accumulation of Africa’s debt:

External borrowing was the single most important determinant of both the timing and magnitude of capital flight from sub-Saharan Africa. Over the 1970–1996 period, roughly 80 cents on every dollar borrowed by sub-Saharan African countries flowed out as capital flight in the same year. This suggests that external borrowing directly financed capital flight ... Capital flight was also a response to the deteriorating economic environment associated with rising debt burdens. The mechanisms by which national resources are channelled abroad as capital flight include embezzlement of borrowed funds, kickbacks on government contracts, trade misinvoicing, misappropriation of revenues from state-owned enterprises, and smuggling of natural resources. [16]

When interest is added, the stock of capital flight in the sample stands at $274 billion, equivalent to 145 percent of the total debt owed by the same group of countries in 1996. ‘In other words’, conclude Boyce and Ndikumana, ‘we find that sub-Saharan Africa is a net creditor to the rest of the world in the sense that external assets, measured by the stock of capital flight, exceeded external liabilities, as measured by the stock of external debt.’ The difference, however, ‘is that while the assets are in private hands, the liabilities are the public debts of African governments’. [17]

All of this would seem to support the claim of Blair’s Commission for Africa that corruption is the single biggest problem facing the continent. Certainly, the private appropriation and reinvestment of loan funds by senior state officials and politicians reached extraordinary heights. Best known is Mobutu Sese Seko, the then dictator of Zaire (now Democratic Republic of Congo), whose personal assets reportedly peaked at $4 billion in the mid-1980s. [18] But simply attributing capital flight to the greed of African politicians hides more than it reveals.

It was, of course, the great powers who propped up African dictators like Mobutu because they guaranteed Western strategic interests during the Cold War. Mobutu was installed in mineral-rich Zaire following the CIA-backed assassination of the popular radical nationalist leader, Patrice Lumumba, and feted by Western governments, corporations and banks for much of his 32-year reign. [19] He and others like him were the creatures of exactly the same people who now cry foul about the endemic corruption of Africa’s ‘political class’.

What is more, the ‘corruption argument’ badly misunderstands the nature of the state in general, and that of Africa in particular. In all post-independence African countries, the state quickly emerged as a site, if not the site, of capital accumulation. Those groups in charge of the state were thus not simply ‘politicians’ and ‘bureaucrats’, but also capitalists. In other words, they were also an economic class and, ultimately, one subject to the exactly same logics and forces as capitalists located in the private sector.

This point is well illustrated by the case of apartheid South Africa. While the likes of Mobutu were shifting capital North in the early 1980s, so too was big South African business. Ben Fine and Zav Rustomjee have estimated that on average as much as 7 percent of GDP per annum left South Africa as capital flight between 1970 and 1988, an equivalent of 25 percent of non-gold imports. [20] This was entirely due to the transfer activities of the major corporations like Anglo-American and the Rembrandt Group. And their behaviour was no less illicit than that of the dictators. Shifting private funds out of South Africa in the 1980s not only defied local capital controls, but broke the international sanctions regime on apartheid. As such, the neoliberal pathologisation of the corrupt black African state simply does not hold. The private ‘white’ capitalists of South Africa were busy engaging in capital flight as well.

Finally, the ‘corruption argument’ tells us nothing about the wider processes that were driving African capital flight. Fine and Rustomjee argue that the South African corporations shifted their resources in response to a combination of declining opportunities for local investment, particularly following the domestic economy’s descent into crisis, and the new opportunities for financial and other investment opening up in the North. [21] This captures the greater truth. Whether Africa’s capital exporters were located in the public or private sectors, they were doing no more than chasing profits – the essence of the entire capitalist system.

The overall situation is thus well summarised by Damien Millet and

Eric Toussaint when they write that ‘debt is a powerful mechanism

for the transfer of wealth from small producers in the South to the

capital-holders of the North, with the dominant classes of the

developing countries skimming off their commission along the way’. [22]

The second distinctive feature of Africa’s debt is the colossal leverage that it has given the Western powers over economies and states. The reason is to be found in the dominant sources of the African debt.

The external debts of Third World countries are usually from a combination of three different types of lending [23]: private or commercial lending by private banks and financial institutions; bilateral inter-government lending by other, mainly Western, states; and multilateral lending by the International Financial Institutions (the International Monetary Fund, the World Bank and its local affiliates like the African Development Bank). Bilateral and multilateral loans are often grouped together and described as ‘public’ or ‘official’ debt.

The vast bulk of Latin America’s debt was derived from financial

markets and in particular US and European banks. As such, Latin

America’s is overwhelmingly a private debt. In contrast, an

increasing majority of African borrowing has come from public

sources, rising from 61 percent in the 1980s to 80 percent by 2003.

[24] The public-private composition of a country’s or region’s

debt is significant because it subjects borrowers to different

repayment conditions, and also different types of ‘debt relief’ scheme.

Private debt: In the 1970s the Western banks responded to the growth of highly liberalised financial markets, the lack of investment opportunities in the depressed advanced economies, and the oversupply of capital (idle Western funds having been boosted by an influx of oil revenues from the OPEC states), by massively increasing their lending to the Third World. [25] The bulk of this credit flowed towards the Newly Industrialised Countries (NICs) of Latin America, Eastern Europe and East Asia where it fuelled a spectacular burst of growth. A far smaller proportion of the new commercial loans also found their way into Africa. Most went to a handful of countries that possessed the strategic raw materials (particularly oil) or existing levels of industrialisation to generate sufficient export revenues to repay the debt. Angola, Nigeria, Congo-Brazzaville, Côte d’Ivoire, South Africa and Zaire were the main destinations. [26] The vast majority of the poorer African states were excluded from this source of credit, although a few of them managed to accumulate relatively small private debts in the 1970s.

This situation was effectively institutionalised after the

official debt crisis broke in 1982. A combination of record high

interest rates, oil price rises and a new world recession meant that

borrowers could no longer generate the export revenues to service

their rapidly escalating debts. The London Club – an organisation

representing the interests of the private creditors – facilitated

the commercial banks’ withdrawal from the Third World debt market

in general and sub-Saharan Africa in particular. With the exception

of the strategic mineral economies, the banks barely lent to the

continent again. Accordingly, private loans only account for around 2

percent of the region’s total debt. [27]

Bilateral debt: The inter-state lending of Western governments was particularly significant in the build-up of Africa’s debt and is the subject of the current Highly Indebted Poor Countries (HIPC) debt relief initiative championed by Brown. What Brown rarely mentions, however, is why the advanced capitalist economies lent so much money to the world’s poorest countries in the first place. The reason is simple: profit.

The Western powers responded to the world recession of 1974–75 with a scheme which tried to boost demand for their home industries by underwriting the export of arms and machinery to the Third World. The liability for this ‘export Keynesianism’ lay with the Third World states themselves. The ‘export credits’ were in reality tied loans that could only be used for the purchase of specified imports. If the Third World country could not cover the costs, the export contract would be honoured by the Western government and converted into a bilateral loan which would either be charged at market interest rates or at (marginally lower) concessional rates and recorded as Overseas Development Assistance (ODA), i.e. aid.

The British, American and other Export Credit Agencies were, like

the commercial banks, gambling on the Third World’s future ability

to repay. Between 1976 and 1980 the Third World’s total debt grew

at an annual average rate of 20 percent through such schemes. [28] In

the end, the gamble failed and the outstanding bilateral loans

accounted for at least a third of the poorest African countries’

total debt. [29] But this did not stop the Western states continuing

to subsidise their arms and other export industries. The Export

Credit Agencies increased their commitments from $26 billion in 1988

to $105 billion eight years later. In 1996 they consequently held 56

percent of developing countries’ official debt. [30] Bilateral debt

has in effect really been killing Africans twice – by underwriting

the export of arms to fuel its many wars, and then by sucking out

desperately scarce resources to ensure that British and other firms

can keep up their lively trade in death.

Multilateral debt: The final portion of Africa’s debt is increasingly owed to the IMF, the World Bank and its affiliates. As a rule, the poorer an African country is, the more likely that these institutions will hold its debt. For example, in 2002 they held 79 percent of Burkina Faso’s debt; 79 percent of Burundi’s; 78 percent of Chad’s; 78 percent of Malawi’s; 81 percent of Rwanda’s and 77 percent of Uganda’s. [31] These debts built up in one of three ways.

The World Bank increasingly lent money to fund ‘development projects’ in the Global South from the 1950s on. A new arm of the bank, the International Development Agency, was established to provide ‘soft’ or ‘concessional’ (i.e. cheap) loans to the poorest developing countries [32], of which fell under the rubric of ODA aid, even though the money had to be paid back. All other project loans were charged at market interest rates. The bulk of the bank’s lending went to major infrastructural projects like power stations or dams. These relied on Western construction companies, consultants and imports, and so they generated a healthy ‘flowback’ – the excess of the profits generated for a member state’s firms over its contributions. [33] There was a particular orientation on financing extractive, export-orientated industries, such as mining, in partnership with private Western banks and multinationals. This was directly tied to the International Financial Institutions’ wider goal of establishing new avenues of accumulation for Western capital in all corners of the globe. [34] Because the World Bank operated like a commercial bank, it was compelled to recover all its debts while continually expanding the number of new project loans, particularly from the late 1960s on. [35] The bank thus emerged as the pre-eminent multilateral institution for facilitating the flow of resources from the South to the North.

The IMF also began to specialise in lending to the Third World, providing short term loans to poor countries in Africa and elsewhere that were experiencing trade deficits (i.e. an excess of imports over exports) and balance of payments crises in the wake of the 1974–75 world recession.

The majority of sub-Saharan African countries were particularly vulnerable to downturns in the world economy because of their reliance on a narrow range of price sensitive primary commodity exports (like cocoa, coffee or copper) – a legacy of colonial rule. The slump of the 1970s saw most raw material prices collapse at a time when the cost of oil imports was shooting up. The IMF began to offer short term loans to ‘stabilise’ these countries’ balance of payments. But harsh ‘conditionalities’ forced borrowers to implement an ‘austerity programme’ of slashing imports, reducing public expenditure and cutting wages in order to reduce their trade deficits and promptly repay the IMF. A second round of oil price rises and even deeper recession deepened the IMF’s hold over the poorest African states. The nominal price of primary commodities fell a staggering 30 percent between 1980 and 1982; in real terms, allowing for inflation, they hit their lowest level since the end of the Second World War. [36] As one African economy after another effectively collapsed, the fund devoted more of its financing facilities to the region. In 1970–78 only 3 percent of the IMF’s new conditional credit went to Africa, but by 1979–80 this figure had shot up to 30 percent. [37]

Both the IMF and the World Bank were able to consolidate their hold over Africa as a direct consequence of the debt crisis. They now assumed a dual role. They ensured that the commercial banks were repaid by lending African states more money to service their private debts. And they acted as debt collection agencies for the Western powers and themselves, working with the creditor governments through the Paris Club. This is an informal grouping of 19 states (Western Europe, Canada, the US, Japan, Australia, Russia) that aims to squeeze the maximum repayments out of the Third World debtors and ensure they don’t default. It divides and rules by insisting all bilateral debts are rescheduled on an individual basis and will only agree to negotiate with a country if it has already signed a debt management agreement with the IMF.

The International Financial Institutions also insisted on the repayment of their own multilateral loans on even harsher terms. The charters of the IMF and World Bank specifically forbid debts that they hold to be rescheduled or written off. Moreover, most of this debt is charged at market rates. [38] This is one of the main reasons why Africa’s total debt has continued to grow while an ever greater volume of resources has flowed out of the continent.

The net effect of the high public composition of Africa’s debt was to overwhelming strengthen the International Financial Institutions’ power.

When the Latin American states came to the brink of default in the early 1980s, the concentration of private bank loans in just three countries threatened to destabilise the entire international financial system by wiping out some of the world’s largest banks. The major powers had no choice but to rush in and attempt to rescue the banks through massive bailouts and schemes designed to shift the burden of repayment onto the shoulders of the workers, peasants and poor.

The African debt was quite different. Not only was it small to the

point of insignificance in world terms, but it was also spread over a

large number of poor countries which had become increasingly

dependent on Western aid as well as loans. As such, individual

defaults did not present much of a threat to the system. [39] This

gave the International Financial Institutions extraordinary leverage

over sub-Saharan Africa and, through this, unparalleled capacity to

launch the neoliberal assault.

The principal levers of the neoliberal offensive were the new Structural Adjustment loans of the World Bank and the IMF. Their overarching aim was, in the words of then US Secretary of State, James Baker, ‘encouraging the private sector and allowing market forces a larger role in the allocation of resources’. [40] This would be achieved through a radical programme of privatisation, liberalisation and reduced public spending that would ‘roll back’ the state and subject the indebted economies to the full rigours of global competition. Structural Adjustment Programmes (SAPs) had effects in Africa over the course of the 1980s and 1990s which significantly shaped the form and content of the debt relief schemes that followed.

But there was immense resistance to the SAPs. Anti-IMF strikes and

riots broke out across the continent in the 1980s and gathered

momentum towards the end of the decade. Protests against the SAPs

turned into struggles against the states that were implementing them.

Between 1989 and 1992 some 20 African countries were rocked by mass

democratisation movements which brought down one government after

another. [50] It is against this background that the debt relief

schemes now hailed by Brown began to emerge.

Gordon Brown’s latest plan for debt reduction slightly modifies the current Highly Indebted Poor Country (HIPC) initiative, which began in 1996. As with so much else New Labour holds dear, the foundations of this scheme were laid by the Tories.

In 1987, the same year that anti-IMF riots swept through Zambia, the then Conservative chancellor Nigel Lawson made a modest proposal to the Paris Club of creditor governments. [51] loans in bilateral aid programmes should be converted into grants; outstanding bilateral debts should be rescheduled; and the rates of interest on some of these loans should be slightly lowered. This was not an act of philanthropy. Lawson was acting on what had become increasingly obvious to the Western powers. The African debt burden had to be reduced so that debt service payments could be maintained to the private banks. In addition to this logic, Lawson’s proposals set out fundamental principles which would be enshrined in all further debt relief schemes. First, only the poorest and most heavily indebted countries would be allowed to qualify; second, all would-be participants would have to adopt and stick to Structural Adjustment Programmes to qualify; and finally, a ‘ring fence’ would be placed round the scheme. On no account were other debtors to be offered any debt relief and, even within the scheme, no debts would be written off.

There was strong resistance to Lawson’s proposals within the Paris Club despite the pragmatism and timidity of the scheme. The US, IMF and World Bank in particular were worried that it would set a precedent and spread from bilateral to multilateral debt. As one US official put it at an IMF meeting, this ‘would completely undermine efforts to persuade debtor nations that major economic adjustment programmes were the key to the eventual resolution of their problems’. [52]

By 1996, however, the World Bank and the IMF were under increasing pressure to shift their position. Mounting resistance to structural adjustment in Africa was combining with an increasingly vociferous campaign by the NGOs to implement full-scale debt relief. At the same time, more African states had failed to meet their debt service obligations, forcing the Paris Club to offer a series of piecemeal concessions which still proved inadequate to keep the payments flowing in. The IMF and the World Bank responded by jointly proposing the Highly Indebted Poor Country scheme which was adopted at the Lyon G7 Summit that year. It marginally reduced the public debt, including the multilateral portion, of the most desperate countries, and it refined the Structural Adjustment Programmes, which, in a typically Orwellian move, were now renamed Poverty Reduction Strategies. All of this was designed to show that the IMF and the World Bank were reforming.

The original Highly Indebted Poor Country scheme proved woefully inadequate and was further ‘enhanced’ in the wake of the massive anti-debt protests led by Jubilee 2000 at the 1998 G7 summit in Birmingham. Gordon Brown and Clare Short declared the enhanced scheme a triumph for New labour’s policy of working for the world’s poor. But, in reality, both versions of scheme were designed to further the neoliberal agenda.

The stated aim is to reduce the debt of the world’s poorest

states to ‘sustainable levels’. This does not mean that it is

writing off all their debt. Rather the International Financial

Institutions attempt to reduce a debt to the point where a country is

out of arrears and is able to sustain its debt service without

recourse to further rescheduling. The scheme is based on three

testing and time consuming stages through which a country must

successfully pass before it is granted any debt relief. Each is

policed by the IMF and the World Bank.

Stage 1: Qualification: To qualify for HIPC, a country must be indebted to an ‘intolerable degree’ and have an established track record of following SAPs. The IMF and the World Bank have determined that only 42 out of 165 developing countries are eligible for the scheme. Thirty four come from sub-Saharan Africa, but a number of heavily indebted African countries are excluded. For example, Africa’s most populous country, Nigeria, has been kept out because, as an oil producer, it is not considered poor enough. This is clearly ludicrous as 70 percent of Nigerians live on below $1 a day. [53]

Each of the 42 countries deemed eligible have had to draw up a Poverty Reduction Strategy Paper with the IMF, containing on average over 100 conditions which are to be strictly followed for three years. These include privatisation and deregulation measures which will hypothetically generate resources to repay the debt, and commitments to use the funds released by debt reduction to reduce poverty. The strategy paper is meant to be drawn up democratically in ‘partnership with civil society’, i.e. local NGOs. But, as a growing amount of research has shown, this is just a rubber-stamping exercise. Throughout the process, power remains with the International Financial Institutions, which hold the veto. [54] It is a continuation of ‘conditionality’ in anything but name.

The IMF and the World Bank use a market-based criterion at the end of the three-year period to calculate whether the ‘economic reforms’ adopted by the country are sufficient to sustain repayment of the debt. The ratio between the present value of debt and projected export revenues has to exceed 150 percent for it to be adjudicated unsustainable. Only then does the country reach the next stage, ‘decision point’.

The criterion used is deeply revealing. The International

Financial Institutions clearly believe that the retention of a large

and costly debt after relief is entirely legitimate. Their

calculation takes no account of the level of poverty in a country,

only its ability to pay. And their projections of future export

earnings are invariably over-optimistic, so significantly reducing

the value of the relief given and forcing the recipients to

renegotiate their debts. [55] It is estimated that eight of the 15

Highly Indebted Poor Countries still at the qualifying stage –

among them Angola, Kenya, Somalia and Sudan – will not be

‘sufficiently indebted’ to reach the next stage at all. [56]

Stage 2: Decision point: A certain amount of interest is

reduced but none of the actual debt is written off for a country that

reaches this stage. It must then pursue implementation of the Poverty

Reduction Strategy Paper in full, which can take a further one to

three years. Mozambique was one of the first to reach this stage.

According to Patrick Bond, its conditions included the privatisation

of municipal water; the quintupling of patient fees for public health

services over a five-year period; and the privatisation and

simultaneous liberalisation of the cashew-nut processing industry at

the cost of some 10,000 jobs. [57] There are currently 18 countries

at the decision point stage.

Stage 3: Completion point: Countries that successfully complete their Poverty Reduction Strategy Paper stage are judged to be ready to have their debt stock reduced. But even this is an illusion. Only the non-ODA (i.e. concessional) proportion of the bilateral debt is reduced. The rest of the bilateral debt stays in place along with the entire multilateral and private debt stocks. Interest payments on the multilateral debt are reduced, but this is only for a fixed period. Some $93 billion of the country’s multilateral debt remains ineligible for cancellation. [58] As such, the nine countries that have reached completion point have remained locked in debt. The G7 promised to write off $100 billion in debt through the HIPC initiative. But since 1996 only $46 billion has been cancelled and this was debt that was never going to be repaid. On average, the initiative will only cut the Highly Indebted Poor Countries’ expenditure on debt servicing by a third. CAFOD have spelt out what this really means for some of Africa’s poorest states:

Mozambique was paying about US$120 billion a year in

interest in principal. After debt reduction, the country will

continue to spend more than US$70 billion a year in debt service. The

reduction in Tanzania’s annual debt service will only be about 10

percent. Cameroon and Zambia, where one in every five children does

not live to see their fifth birthday and their parents earn less than

60 cents a day, will be left with a combined debt stock of nearly

US$5 billion. [59]

So where do Brown’s new proposals fit in with this massive con? The Brown initiative has generally been headlined as ‘100 percent debt cancellation for the world’s poorest countries’. This is well off the mark.

Multilateral debts held by the World Bank: Brown hopes to

persuade the other G8 states to donate additional funds to cover the

World Bank’s lost debt service revenues from the eligible

countries. In Britain’s case, a pledge has been made to cover 10

percent of the bank’s loss. Yet this money will also count towards

Brown’s much vaunted increase in Britain’s aid budget. [61] As

such, it is taking away resources that would otherwise have flowed

into the South as aid. The US has tabled a counter-proposal that the

World Bank cancels 100 percent of the debts owed by all 42 HIPC

countries, but recovers the lost debt service revenues by taking the

money out of their aid allocations. This, as NGOs have pointed out,

‘effectively involves making poor countries pay for their own debt

relief’. [62] Whatever their differences, then, it is clear that

both Britain and the US are determined that under no circumstances

will multilateral debt relief come for free.

Multilateral debts held by the IMF: Brown has proposed that the IMF sells off part of its huge gold reserves to cover the reduction in debt service payments it receives. But there would be strong opposition in the US Congress to the cost of such a move [63] and the powerful Gold Council has vigorously lobbied the US Treasury against it, fearing it will flood the market and lead to a fall in the world gold price. For the same reason, there are also reported splits at the cabinet level in South Africa, one of the largest gold producers in the world. [64]

In a sense, the intense speculation over which is the better of the rival debt relief schemes is superfluous. If the G8 were serious about writing off Africa’s debt they could do it at a stroke. There was, for example, no problem cancelling Iraq’s $120 billion debt when it suited their interests after the invasion in 2003. At the time, Bush argued that Iraq’s liabilities endangered its ‘long-term prospects for political health and economic prosperity’. [65] This is true of Africa’s debt a thousand times over.

As the Senegalese activist Debar Moussa Dembele makes clear, the African debt has a purpose: ‘It is an instrument of domination, control and plunder, used to promote Western countries’ economic, political and strategic interests.’ [66]

There is only one way to show real solidarity with Africa and the Global South. Demand that the entire Third World debt – multilateral, bilateral and private – is dropped, with no strings attached. This directly challenges the power of the exploiters, crooks and killers gathering at the G8 Summit to plan their next phase of global impoverishment and war.

The terms Third World, Global South and South are used interchangeably in this article.

1. World Bank, Global Development Finance, 2005.

2. R. Greenhill and A. Pettifor, The United States as a HIPC – How the Poor are Financing the Rich, Jubilee Research and New Economics Foundation Report (2002), p. 3.

3. A. Callinicos, An Anti-Capitalist Manifesto (London 2003), p. 28.

4. S. Riley, Debt, Democracy and the Environment in Africa, in S. Riley (ed.), The Politics of Global Debt (Basingstoke 1993). p. 114.

5. Ann-Louise Colgan. Africa Action Position Paper: Africa’s Debt (July 2001), p. i.

6. United Nations Conference on Trade and Development (UNCTAD). Debt Sustainability: Oasis or Mirage?, Economic Development in Africa Series (2004), p. 6.

7. As above, p. 5.

8. P. Bond, Against Global Apartheid: South Africa Meets the World Bank, IMF and International Finance (Cape Town 2001), p. 21.

9. J. Boyce and L. Ndikumana, Africa’s Debt: Who Owes Whom?, Political Economy Research Institute Working Paper Series, 48 (2002), p. i.

10. P. Bond, as above, p. 22.

11. A. Pettifor, Debt, in E. Bircham and J. Charlton (eds.), Anti-Capitalism; A Guide to the Movement (London 2001), p. 48.

12. K. Owusu et al., Through the Eye of a Needle: The Africa Debt Report, Jubilee 2000 Coalition Reports (London 2000), p. 6.

13. J.K. Boyce and L. Ndikumana, Africa’s Debt: Who Owes Whom? (2002), p. i.

14. Cited in Ann-Louise Colgan, as above, p. i.

15. J. Boyce and L. Ndikumana, as above, p. 2.

16. As above, p. 3.

17. As above, pp. 2–3.

18. As above, p. 3.

19. For a brief account of the relationship between Mobutu, the banks and Zaire’s debt, see S. George, A Fate Worse than Debt (London 1990), pp. 106–118.

20. B. Fine and Z. Rustomjee, The Political Economy of South Africa: From Minerals-Energy Complex to Industrialisation (London 1996), p. 177.

21. As above, p. 247.

22. D. Millet and E. Toussaint. Who Owes Who? Fifty Questions About World Debt (London 2004), p. 87.

23. ‘Debt’ here denotes the external public debt of the developing countries. That is, the debt which is owed or guaranteed by Third World governments, as opposed to that owed by private enterprises in the Third World, which is termed the external private debt.

24. UNCTAD, as above, p. 3.

25. A. Callinicos, Imperialism Today, in A. Callincos et al., Marxism and the New Imperialism (London 1994), p. 35.

26. Until 2004 just two countries, Angola and Nigeria, accounted for 53 percent of all FDI in sub-Saharan Africa (now down to 36 percent) with the rest concentrated on South Africa. World Bank, Sub-Sahara Africa Summary, Global Development Finance 2005, p. 4.

27. E. Toussaint, Your Money or Your Life! The Tyranny of Global Finance (London 1999), p. 198.

28. As above, p. 84.

29. Jubilee Research, Debt by Donor in Nominal Values (2002), at www.jubileeresearch.org. [Note by ETOL: No longer online]

30. According to the international ECA Reform Campaign. Cited in S. Bracking, Regulating Capital in Accumulation: Negotiating the Imperial Frontier, Review of African Political Economy 95 (2003), p. 21.

31. Jubilee Research, Debt by Donor ..., as above.

32. The real impetus for the IDA was the need to outflank a rival initiative proposed by Third World states via the UN. Although the World Bank had little time for soft loans, the IDA would ensure that multilateral development lending remained under the North’s control. W. Bello, Deglobalization: Ideas for a New World Economy (London 2004). p. 37.

33. Flowback is the bank’s own term. To give an idea of its magnitude, Eric Toussaint cites a speech by Belgium’s executive director at the World Bank and the IMF to the Belgium employers’ federation in 1986: ‘Flowback ... has risen seven to ten for all industrialised countries taken together. Which means for every dollar put into the system, industrialised countries got back seven in 1980 and 10.5 now’. E. Toussaint, Your Money or Your Life!, as above, p. 131. The ghastly history of the World Bank’s project lending has been well documented. Susan George and Fabrizio Sabelli provide a good overview – Faith and Credit: The World Bank’s Secular Empire (London 1994) – while Patrick Bond catalogues pertinent Southern Africa examples old and new – Against Global Apartheid, as above, pp. 61–67; and Unsustainable South Africa: Environment, Development and Social Protest (London 2002).

34. A good example of this process was the World Bank’s part-funding of infrastructure to support the development of the Selebi-Phikwe copper/nickel mine in Botswana in the 1960s. J. Parson. Botswana: Liberal Democracy and the Labour Reserve in Southern Africa (London 1984), pp. 75–76.

35. According to Eric Toussaint, ‘During the first 22 years of its existence, the World Bank provided loan financing for only 708 projects, to the tune of $10.7 billion. From 1968 onwards, however, loan totals skyrocketed. Between 1968 and 1973, the World Bank loaned $13.4 billion for 760 projects.’ E. Toussaint, Your Money or Your Life!, as above, p. 82.

36. P. Green, Debt, the Banks ..., p. 27.

37. L. Harris, The Bretton Woods System and Africa, in B. Onimode (ed.), The IMF, the World Bank and the African Debt: The Economic Impact (London, 1989), p. 9.

38. According to the World Bank in 1989, around 3O percent of Africa’s total debt, including short term credits and drawings from the IMF, was set at commercial rates. World Bank, Sub-Saharan Africa – From Crisis to Sustainable Growth (Washington 1989). p. 21.

39. This point is made by no less a party than the World Bank, in sub-Saharan Africa, as above, p. 22; and echoed by Colin Leys, Confronting the Africa Tragedy, New Left Review 204 (1994), p. 36.

40. Cited M. Hall, The International Debt Crisis: Recent Developments, Capital and Class (1988), p. 8.

41. By 1990, 30 out of the 45 states in sub-Saharan Africa had some form of SAP in place. S. Riley, Debt, Democracy and ..., as above, p. 117.

42. The first figure is taken from E. Toussaint, Your Money or ..., as above, p. 197; and the second from J. Saul and C. Leys, Sub-Saharan Africa in Global Capitalism, Monthly Review 51 : 3 (1999).

43. According to Patrick Bond, ‘sub-Saharan African manufactured products fell steadily from 18 percent of GDP in 1970 to 15 percent by 2000, while gross capital formation crashed from a peak of 25 percent of GDP in 1980 to just 15 to 18 percent during the subsequent decade (compared to China’s steady 35 to 40 percent over the same period)’. P. Bond, Bankrupt Politics: Imperialism, Sub-Imperialism and the Politics of Finance, Historical Materialism 12 : 4 (2004), p. 159.

44. Bond continues, ‘From 1980 to 2000. cotton prices fell by 47 percent, coffee by 64-percent, cocoa by 31 percent and sugar by 77 percent. Africa’s agricultural exports were down from US$15 billion in 1987 to US$13 billion in 2000.’ As above, pp. 158–159.

45. World Bank, Sub-Saharan Africa – as above, p. 7.

46. UNCTAD, Economic Development in Africa: Performance, Prospects and Policy Issues, Economic Development in Africa Series (2001), pp. 5 & 7.

47. World Development Movement (WDM). Zambia: Condemned to Debt-How the World Bank and IMF have Undermined Development, WDM Parliamentary Briefing (May 2000), p. i.

48. See, for instance, the figures for real wages in Africa Unemployment Report 1990 (Addis Ababa 1991), pp. 35–39.

49. See for example M. Mackintosh, Questioning the State, in M. Wuyts et al. (eds.), Development Policy and Public Action (Oxford 1992).

50. For useful overviews, see C. Allen et al., Surviving Democracy?, Review of African Political Economy 54 (1992): and L. Zelig and D. Seddon, Marxism, Class and Resistance in Africa, in L. Zelig (ed.), Class Struggle and Resistance in Africa (Cheltenham 2002).

51. M. Hall, The International Debt Crisis: Recent Developments, Capital and Class 35 (1988), pp. 14–15.

52. Cited in M. Hall, as above, p. 8.

53. World Development Movement, The Non-HIPCs: Indebted, Excluded and Poor, WDM Debt Resources (2000), p. 2.

54. For revealing accounts of what NGO ‘participation’ really means, see P. Bond, Talk Left, Walk Right: South Africa’s Frustrated Global Reforms (London 2004). pp. 80–85.

55. CAFOD, The Rough Guide to Debt, A CAFOD Briefing (n.d.), p. 4.

56. Jubilee Debt Campaign, What’s Wrong with HIPC?.

57. P. Bond, Against Global ..., as above, p. 74.

58. Jubilee Debt Campaign, Facts and Figures.

59. CAFOD, The Rough Guide ..., as above, p. 4.

60. World Development Movement, Africa Set to Gain Little from UK in 2005, WDM Press Release, 30 December 2004.

61. World Development Movement, Short Measures: Why the UK Government Proposals Won’t End the Third World Debt Crisis, WDM Media Briefing, 16 May 2005.

62. Jubilee Debt Campaign, Action Aid and Christian Aid, In the Balance: Why Debts Must be Cancelled Now to Meet the Millennium Development Goals, Joint NGO Media Briefing Paper for World Debt Day, 16 May 2005.

63. A. Balls et al., IMF Weighs Gold Sales Options, Financial Times, 1 February 2005.

64. J. Fraser, Worried SA to Speak to IMF about Gold Sales, Business Day, 10 February 2005.

65. Cited in M. Engler, Debt Cancellation: Historic Victories, New Challenges, Foreign Policy in Focus Special Report, May 2005.

66. D. Moussa Dembele, Toronto, Naples, Lyon, Cologne and London: G7 Leaders and the Debt Trip to Nowhere, Pambazuka News, 10 March 2005.

ISJ 2 Index | Main Newspaper Index

Encyclopedia of Trotskyism | Marxists’ Internet Archive

Last updated on 13 January 2017