Movement of Wholesale Prices and Weekly Wages, 1800-1932

Main ISR Index | Main Newspaper Index

Encyclopedia of Trotskyism | Marxists’ Internet Archive

From International Socialist Review, Vol.19 No.3, Summer 1958, pp.93-98.

Transcription & mark-up by Einde O’Callaghan for ETOL.

|

Study of the long-range trend suggests that rising prices, despite the dips, are a built-in feature of capitalist economy This is the first part of an article submitted to the International Socialist Review for discussion by those of its readers who are interested in the problem of long-range inflation. Albert Phillips is a Detroit trade unionist. |

* * *

ONE of the major historical and theoretical characteristics of healthy and expanding capitalism was its ability to constantly cheapen commodities. Through the “heavy artillery” of its low prices it was able to batter down the “Chinese Walls” of backward nations and “create a world after its own image.” [1]

But it is not only in regard to conflict with other social formations that the cheapening of commodities is important. Within the confines of the system itself, from the point of view of the individual capitalist or capitalist nation, it is the peaceful means of capturing a larger share of the internal market in the first instance, and of the world market in the second. More important than the capture of a larger share of a given market was the expansion of the indeterminate market. Along with the lowering of prices went a tremendous expansion of production and accumulation of capital. Along with the concomitant growth of the proletariat and the sharpening of the class struggle came an increase in real and money wages, a shortening of hours, and a general improvement in living standards. Thus on the whole, the period associated with falling prices is also of necessity an epoch of internal expansion of the market for capital goods and for consumer goods despite the periodic crises.

We note that on a social scale the cheapening of wage goods increased relative surplus value; and, in addition, by lowering the cost of capital goods a countertendency to the falling rate of profit was set up.

In his own way Joseph Schum-peter, one of the foremost non-Keyne-sian economists in the bourgeois world, recognized the central importance of this feature of capitalism when he wrote that

“Experience tends to show, however, that neither capitalism itself nor the social institutions associated with it, democracy among them, can work with efficiency and with comparative smoothness except on a falling trend in prices.” [2]

As a long-range movement, however, the period of capitalism associated with a falling trend in prices ended with the close of the nineteenth century. It has since that time been replaced by a secular inflationary tendency which has been accelerating until today it threatens to break out of control on a world-wide scale and bring the capitalist credit structure, and with it the bourgeois mode of production, crashing about the ears of the bourgeoisie.

Secular inflation is indeed not the antipode of the stagnation manifested in the thirties; it is a different but equally dangerous indication of the underlying sickness. The flush of the inflationary boom is not a sign of health but a warning as in tuberculosis of impending disaster. It is a form manifesting the basic contradiction in capitalism, the declining rate of profit, through the operation of which capital itself becomes the ultimate barrier to capitalist production.

That the bourgeoisie senses the fatal character of the disease, although it is incapable of either explaining or treating it, is evident in the continuing debate which is taking place all over the capitalist world. The dispute is dominated by the intellectual offspring of the depression, the Keynesian and neo-Keynesian advocates of a “mild” and state-managed inflation as the antidote to stagnation.

Despite their dominant position, they too are at loggerheads among themselves. In itself this is not surprising, for it was after all Keynes himself who wrote:

“Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction,, and does it in a manner which not one man in a million is able to diagnose.” [3]

The fact is that the inflationary process is developing according to its own laws, and is close to the stage feared by Keynes. It is beyond the point of serving as an instrument for encouraging production while at the same time providing a relatively painless way of extracting more surplus value from the working class.

The dispute itself has developed some ironic twists. In England the Keynesian leadership of the trade-union movement has condemned the government for failing to sufficiently stimulate investment in capital goods. [4] On the other hand Sir Dennis Robertson, an advocate of mild doses of inflation, has recently stated the necessity of accepting stagnation in the accumulation of capital, since growth, in his opinion, can be achieved only at the expense of further inflation. [5] This is an extremely important empirical conclusion to which we shall return. But on this side of the Atlantic it is mostly the Keynesian welfare-state economists, along with labor leaders like Reuther, who hold that there is too much investment [6], and that the cause of inflation can be found in “administered prices” designed to permit expansion of capital from internal sources. [7] It is the spokesmen for Big Business, on the other hand, who hold that there is insufficient capital growth, that productivity is not rising fast enough, and that profit margins are being squeezed. [8]

The growing bewilderment of the economists is over the character of an inflation which defies their universally accepted axioms. Inflation continues despite a falling off of demand. It develops even with the growth of excess capacity in many important industries. It is accelerating even in the teeth of increasing unemployment. [9] In short, it defies the rules of their textbooks which teach that inflation occurs because of lack of goods to supply effective demand.

Nevertheless, the majority of economists who testified at the Congressional hearings in Washington in June and July of 1957 were able to convince themselves, despite their acknowledged bewilderment, that high wages are at the bottom of the present inflation. [10] More typical today in the long run are those who lay blame equally on “big labor” and Big Business for the inflationary spiral. [11] Thus, while many of the Keynesians have stressed wages, some have emphasized administered prices and some have pointed to both, it is noteworthy that they have not referred to the role of the government and the government debt. Only some of the more unreconstructed elements among the bourgeoisie, who as yet fail to accept the irrevocably increasing role of the state in the capitalist economy, have pointed an accusing finger in this direction. [12] As could be expected, it has been the labor bureaucracy and welfare-state economists like Dr. Edwin G. Nourse who have defended the role of the government against all comers. [13]

This “oversight” becomes rather glaring when we note that taxes take, directly or indirectly, more than a third of the average worker’s income and close to 50% of corporate profits; that one out of every eight persons is employed by the government; that one out of every five dollars of the country’s assets is in government property (even excluding federal highways and military equipment); that one out of every 20 dollars in all business sales is made to the government; that the $72 billion federal budget for 1958 is three times greater than all corporation net profits in 1956. It is worth observing too that 88 cents out of every budget dollar is directly or indirectly related to war. Facts such as these indicate why capitalist politics has become ever more inseparable from capitalist economics, just as politics in general has become increasingly intertwined with economics.

We are not in this article concerned with weighing the class bias at the bottom of the differing evaluations of the cause of the inflation, although, as we shall indicate below, the approach which equates wages with that of profits and interest as equal causes is factually untenable. Nor are we presently concerned with the manner in which Reuther, in his proposal to reduce the demands of auto workers if the corporations reduce prices, accepts the crudest ideology of the ruling class. We are for the moment more interested in the fact that the opposing elements proceed from a common acceptance of the capitalist system. This is the basis of the confusion.

If we were to compound all their explanation for inflation, even though each might contain a measure of validity, we would not be much further ahead. The inability of the economists to agree on the cause has led the National Planning Association to declare that the difficulty lies in insufficient facts. [14] But the reality is that American bourgeois economists above all others are slowly strangling in a bog of statistics. It would take pages simply to list the periodicals, the special studies, and the newly formed groups which are pouring out statistics by the yard. The major difficulty is that the figures deal with static relations, mathematical equations for equilibrium situations, or with short-run trends. Only a few economists of stature have cared to tackle the long-run developments, because here a selective theory is necessary and any theory that goes below the surface is dangerous to those who would uphold capitalism. Men like Simon Kuznets, Joseph Schumpeter and the Englishman Colin Clark are in a decided minority. It is not accidental that Schumpeter reluctantly found his investigations leading to the conclusion that capitalism is doomed.

After we have established the secular movement of prices over the past 150 years, we shall then be in position to ask why capitalism in the twentieth century is no longer capable of the achievements of a progressive and expanding economy; why it is no longer capable of simultaneously lowering prices, increasing both monetary and real wages, shortening the work week and thereby expanding the market and increasing production at a growing rate.

The major fact with which our discussion begins is that the course of prices, beginning roughly with the end of the eighteenth century, shows a clear downward slope after allowing for temporary oscillations, generally associated with wars in the upward direction and with crises in the downward swing. Contrary to those who attempt to trace the inflation from 1939, or 1947, or 1954, the general upward movement in prices begins roughly with the end of the nineteenth century, the beginning of the epoch of the death agony of capitalism.

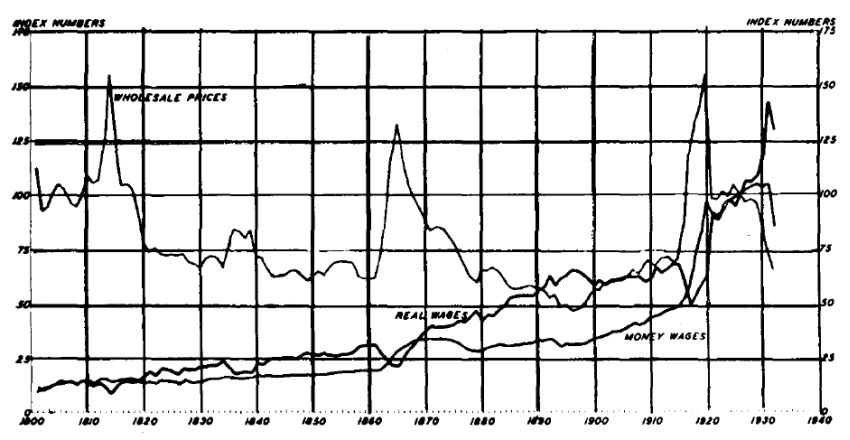

We present a graph of the movement of prices in the United States from 1800 to 1932 [15] to which we add data below to bring it up to date.

|

Movement of Wholesale Prices and Weekly Wages, 1800-1932 |

|---|

| |

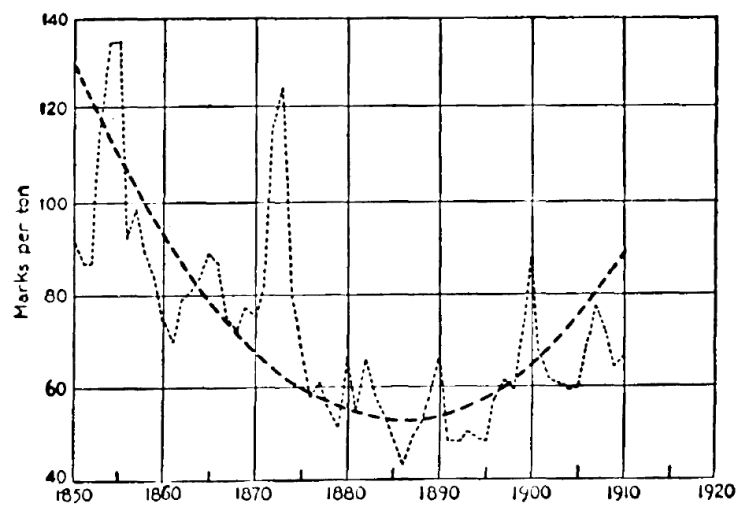

If this graph were to be transformed in the manner generally used by statisticians to develop trend lines; i.e., after smoothing the series with a moving average plotted on a Gompertz curve, it would show a concave parabola. We give as an example the curve developed for the price of pig iron in Germany, 1850-1910, by Dr. Simon Kuznets. [16]

|

Prices of Pig Iron, Germany, 1850-1910, |

|---|

|

We have selected this commodity because the curve of its price movement is relatively typical of the great number of key commodities which were analyzed by Kuznets for most industrialized countries.

In our first graph, if we take 100 as the index figure for 1800, by 1895 wholesale prices dropped to around 45, then began their rise and by 1900 reached about 52. If we extend the series beyond the years shown in the graph, with 1900 as 100, the rise came to 265 in 1947. [17] A further extension made in terms of the purchasing power of the dollar with its index at 100 in 1939, shows it down to 49.8 in April of 1957. [18] In the eighteen-month period through September 1957, the cost of living went up 5.6%, probably the steepest inflationary movement in any period not directly associated with war. [19]

Thus the slope of the parabola for the total movement of prices over the entire period would be somewhat different from that shown for pig iron in the more limited period. The downward slope from 1800 to 1895 would be more gradual, as would the rise to 1939. After that the angle of the slope would begin to move upward in an increasingly sharp manner.

There are some additional aspects of the first graph which are of interest. In the first place we note that in the later period the upward oscillations go higher while the downswings do not drop as low as in the earlier period. For example, with 1900 as 100, the index figure for the lowest point in the depression years of the thirties stands at 123. This again clearly emphasizes the character of the underlying long-range pull.

Secondly, we should note that although there is undoubtedly some variation in the dates and the angles of slope, the general form of the movement is valid for the entire industrialized world. The Kuznets studies referred to above bear this out as does the chart which is presented below.

In the third place it is important to observe that the secular upward swing began before war preparations and the state debt became a major factor, thus underlining the fact that the tendency to inflation is rooted directly in the nature of capitalist production as such. In contrast to World War II, there was no real economic mobilization for World War I even in Germany.

“In 1913, Germany’s military expenditure, which had then been very considerably increased as compared with previous years, amounted to approximately ... 4% of Germany’s national income.” [20]

In order to emphasize the sharp breaking point, characteristic of the turn of the century before the state debt began to become an important factor, and in order to illustrate the worldwide nature of the movement of prices, we introduce figures for this period from another source. [21]

|

Index of Prices 1890-1911 |

||||||

|---|---|---|---|---|---|---|

|

Average |

UK |

UK |

France |

Germany |

USA |

Canada |

|

1890-99 |

100 |

100 |

100 |

100 |

100 |

100 |

|

1900-09 |

104 |

111 |

109 |

115 |

118 |

115 |

|

1910 |

113 |

118 |

118 |

128 |

132 |

125 |

|

Sept. 1911 |

– |

122 |

126 |

139 |

– |

– |

It will be noted that the two countries showing the greatest inflationary leap, Germany and the United States, were the two most actively accumulating capital and expanding production in this period. It is worth repeating that preparations for war did not play any role, nor did the state debt. In any case it would seem clear that the inflationary process began with the twentieth century and not, as the bourgeois economists would have it, with 1939 or 1947. [22]

Prices of finished commodities, of course, despite their importance as the manifestation of underlying developments in production, are not the only matters which concern us. There are other allied characteristics of nineteenth century capitalism whirh are in sharp contrast to that of the twentieth centurv. These are commonly known, and for the present we need do no more than mention their existence in the context of this article. We have indicated that not only was expanding capitalism able to lower prices, but simultaneously to expand the market, to expand production, profits and the accumulation of capital, to absorb lowering of the hours of work, and to increase both real and money wages over the long run. And while we deal mostly with American capitalism, the same general tendencies can be observed throughout the industrialized world.

In England during the early 1800s, for example, hours of work went as high as 19 to 20 a day, and 90 to 100 a week. In 1842 the work day in the English mines was 14 to 15 hours a day, not only for men, but for women and children. In 1840 the normal work week in Massachusetts textile mills was 84 hours. By and large the campaign for the 10-hour day lasted until the middle of the 1890’s. [23] On this question, as with that of wages, the rate of advance depended upon the state of organization and militancy of the working class. We are at the moment, however, more interested in demonstrating the relative economic viability of capitalism in the nineteenth century.

Wages, both real and money, showed a slow but steady increase. With money wages at 11.0 in 1801, by 1900 they reached 32.6; with real wages at 9.8 in 1801, by 1900 they reached 58.1. [24]

The value of manufactured products, including the period which witnessed the greatest drop in prices, increased in millions of dollars from 1,019 in 1849 to 13,000 in 1899 [25], thus indicating the expanding character of capitalism in this general area as well.

How then can we explain the qualitative change in character between the capitalism of the nineteenth and of the twentieth century as it is summarized in the dramatic change in the direction of prices? It is my contention that the explanation lies in the falling rate of profit along with the positive effects of the class struggle; and that the growth of debt, including state debt, and the growing intervention of the state in the economy are increasing contributory effects rather than prime causes.

The rate of profit depends, as we know, upon the relationship between constant and variable capital. It tends to fall as the organic composition of capital goes up, assuming that the rate of surplus value remains constant. Thus in considering the actual course it is not enough simply to establish that constant capital increases over variable. Two other ratios must be considered. In the first place there is the ratio of the proportional change in the organic composition of capital to the resulting proportional change in labor productivity. In the second place we must watch the ratio of this change in labor productivity to the resulting increase in relative surplus value, achieved through a fall in the price of wage goods, a consequent fall in money wages, and a consequent rise in the rate of surplus value. [26] As far as the second ratio is concerned, the effects of the class struggle cannot be separated from the purely economic result.

Let us turn our attention first to the ratio of the proportional change in the organic composition of capital to the resulting proportional change in labor productivity. Dr. Simon Kuznets, after a careful and lengthy study concludes that

“The information scattered in the histories of industries seems to indicate that the ratio of net returns to capital invested is larger in the early periods of growth. When a branch of production is just beginning to develop successfully ... the returns to the pioneers are, in proportion to the size of the actual investment, much larger than later on, when the industry achieves bulk and stability. The chief reasons for these large returns during early growth seem to lie in the rapid rate of technical change, rapid improvement of the product, and lowering of costs.” [27]

We are struck by the similarity between the findings of Kuznets and the comments of Marx: “This opening period [extension of machinofacture into industries dominated by old-time handicrafts or manufacture], in which the machine is achieving the conquest of its sphere of activity, is of decisive importance owing to the extraordinarily high profits which can be made at such a time. These profits do not only form a source of accelerated accumulation; for they also attract into the favoured sphere of production a large part of the additional social capital which is being constantly created, and is ever on the lookout for new investments.” [28]

The following examples constitute prima facie evidence that the leap in labor productivity far outdistanced the proportional change in the organic composition of capital. The first example is taken from the cotton industry of England. [29]

|

Price of Yarn |

||

|---|---|---|

|

|

Shillings |

Pence |

|

1779 |

14 |

0 |

|

1784 |

8 |

11 |

|

1799 |

4 |

2 |

|

1812 |

1 |

0 |

|

1830 |

0 |

6.8 |

|

1860 |

0 |

6.3 |

|

1882 |

0 |

3.4 |

We note first that the marked and continuing decline in prices illustrates in microcosm the general course of price tendencies in the nineteenth as against the twentieth century. But in addition, in commenting on the table, Kuznets points out that the rate of decline in the cost of capital and labor per unit of production has been diminishing, and whereas for the first 51 years the cost of yarn 40 hanks to the pound declined 96%, for the next 50 years it declined only 50%. That is, the increase in labor productivity tends to decline in proportion to the organic change in the composition of capital.

Our second example, taken from America, deals with steel rails produced by the Carnegie Steel Company. [30]

|

|

Average Monthly |

|

Price Received |

|---|---|---|---|

|

1875 |

$57.00 |

$66.50 |

|

|

1878 |

38.00 |

42.50 |

|

|

1883 |

34.00 |

37.50 |

|

|

1888 |

28.00 |

29.83 |

The continued decline in the price of steel, along with the decrease in the rate of decline, are evident here as well as in the first example. It will be rewarding to refer to these figures when we later discuss the modern steel industry in relation to price tendencies. It is also important to note that while using only his personal resources, Carnegie in the 11 years from 1889 to 1900 was able to finance the expansion of production from 322,000 tons to 3,000,000. At this point there appears yet another similarity between the theory of Marx and the empirical findings of Kuznets, who says that

“the funds available for the expansion of an industry decrease in relative size as the industry grows ... the rise of a new industry or the revolutionary expansion of an old one implies a considerable new investment. Capital must be provided either from the returns of the industry concerned, or from the returns (or possibly capital) of the other industries. Considering for the present only subsidies from the outside, it seems clear that the funds available relative to the size of the subsidized industry are greater in the earlier periods than later on.” [31]

The key phrase here is the availability of profits relative to the size of the capital to be expanded. Measured in terms of the accumulation of capital, the tendency of the rate of profit to decline is the Marxist way of saying that the amount of profit available, relative to the existing stock which is to be expanded, tends to lessen. In the third volume of Capital Marx points to the necessity of the accumulation of capital in geometric fashion in order to overcome the declining rate. But it is precisely the declining rate which cuts into the possibility of geometric expansion, unless there are qualitative leaps in the productivity of labor relative to the proportionate increase in investment in capital goods, a relationship which came into being in the era of the Industrial Revolution and which ran its course by the end of the nineteenth century.

No one can for a moment today imagine that one individual, however rich, would be capable of undertaking expansion such as Carnegie carried through. But we must leave for later consideration the effect of the ever-widening search for sources of capital upon the creation of fictitious capital and debt, as well as the growing need to socialize credit and debt through the mechanism of the banks and the state itself. We leave also for later comment the effect of the declining rate of profit on the possibility of a new industrial revolution under capitalist auspices.

Before we begin our discussion of capitalism in the twentieth century, some additional comments illustrating the character of the previous century will prove of value, above all now that the movement for a shorter work week with no cut in pay is coming to the fore. Marx, in the course of his debate with Weston, wrote:

“... I propose calling your attention to the real rise of wages that took place in Great Britain from 1849 to 1859. You are all aware of the Ten Hours Bill, or rather ten and a half hours bill, introduced since 1848. This was one of the greatest economic changes we have witnessed. It was a sudden and compulsory rise of wages, not in some local trades, but in the leading industrial branches by which England sways the markets of the world ... Well, what was the result? A rise in the money wages of the factory operatives, despite the curtailing of the working day, a great increase in the number of factory hands employed, a continuous fall in the prices of their products, a marvellous development in the productive powers of their labor, an unheard of progressive expansion of the markets for their commodities ... I proceed to state that from 1849 to 1859 there took place a rise of about 40 per cent in the average rate of the agricultural wages of Great Britain ... Despite the Russian War, and the consecutive unfavorable harvests from 1854 to 1856, the average price of wheat, which is the leading agricultural produce of England, fell ... This constitutes a fall in the price of wheat of more than 16 per cent simultaneously with an average rise of agricultural wages of 40 per cent.” [32]

Such a combination of developments as Marx has described is unthinkable today, although it was not, as we have earlier indicated, unusual in the nineteenth century. The key here remains the “marvellous development” of the productive power of labor in proportion to the investment in capital.

Nevertheless, as we have observed, there would seem to be even in the nineteenth century a tendency for the ratio, established by the proportionate increase in the organic composition of capital to the increase in labor productivity, to increase. To use more current terminology, it might be said that the marginal efficiency of capital has tended to decline, the capital coefficient has tended to increase, or the capital-output ratio has tended to go up.

Harold Moulton of the Brookings Institute declares: “The fact that prices as a whole declined during the nineteenth century suggests that the general increase in productivity was more than sufficient to meet the increasing cost of wages.” [33] The statement is somewhat lopsided, since it tends to focus attention on wages as the major factor in price scales. Nevertheless, with this proviso, it points to the second decisive ratio with which we began our discussion, the ratio of the change in labor productivity to the resulting increase in surplus value. Here the facts indicate a growing tendency toward inflexibility – a tendency for both real and money wages to rise along with the shortening of the work week.

Thus the bourgeoisie entered the twentieth century with gradually increasing pressure exerted on one side by the falling rate of profit and on the other by the widening organization and resistance of the working class. The economic result is inflation.

The alternatives available to the capitalist rulers would seem to boil down to either crushing the resistance of the working class, or developing a new industrial revolution which would produce a great qualitative leap in the productivity of labor in proportion to capital investment. The latter alternative would permit them to temporarily overcome the tendency to a declining rate, and would open the possibility for a new period of expansion. Is a new industrial revolution under capitalist auspices possible? The answer, which will be developed in the second part of this discussion article, is a clear negative.

1. Communist Manifesto (Kerr ed.; 1911), p.19.

2. Schumpeter, Business Cycles (McGraw-Hill Book Co., Inc., New York, 1939), II, 465.

3. As quoted by Prof. M. Bronfenbrenner in Post-Keynesian Economics, edited by K. Kurihara (Rutgers University Press, New Brunswick, N.J., 1954), p.31.

4. New York Times, August 20, 1957.

5. New York Times, September 7, 1956.

6. Report made by Leon Keyserling, former “Chairman of the Council of Economic Advisers to President Truman, for the Conference on Economic Progress (of which Reuther is a member). The report also condemned the cutback in military expenditures. Detroit News, September 9, 1956.

7. Statement adopted by the AFL-CIO Executive Council. New York Times, August 15, 1957.

8. Dr. Ralph Robey, A New Force for Inflation (pamphlet issued by the National Association of Manufacturers). Robey is the NAM’s chief economist.

9. New York Times, June 27, 1957. See also Prof. Sumner Slichter, New York Times, August 8, 1957, and Arthur Krock, New York Times, June 7, 1957.

10. New York Times, June 6, 1957, for example. Economists involved were Walter Heller of the University of Minnesota, William J. Fellner of Yale, Paul Samuelson of the Massachusetts Institute of Technology.

11. For example, Dr. Edwin G. Nourse of Brookings Institute, another former Chairman of Truman’s Council of Economic Advisers. In an address before the National Citizens Committee to Curb Inflation, he attacked “tricky gadgets’’ such as administered prices fostered by Big Business and the escalator and annual improvement-factor clauses demanded by labor. New York Times, June 25, 1957. In testifying before the Kefauver Committee he also attacked as inflationary the demand for a shorter work week with no reduction in pay.

12. For example, General Douglas MacArthur, now president of the Sperry-Rand Corporation. In remarks at a meeting of stockholders he declared that the threat of taxation is greater than the danger of war with the Soviet Union. The Freeman, January 1957.

13. An editorial Strangling the Welfare State in the August 1957 United Auto Worker boasted: “Only a few weeks ago the labor movement and the liberal Democrats were defending the President’s budget against Congressional cuts.” This budget contained the greatest peacetime appropriations for armaments in American history. Dr. Nourse, in testifying before the Kefauver Committee, defended the policies of the Eisenhower administration while attacking labor’s demand for a shorter work week.

14. New York Times, April 1, 1957.

15. Harold G. Moulton, Income and Economic Progress (Brookings Institute, Washington, D.C., 1935), p.107.

16. Kuznets, Secular Movements in Production and Prices (Houghton Miflin Co., New York, 1930), p.153.

17. Harold G. Moulton, Controlling Factors in Economic Development (Brookings Institute, Washington, D.C., 1949), p.280.

18. Statement by George M. Humphrey, Secretary of the Treasury, before the Senate Finance Committee. New York Times, June 19, 1957.

19. New York Times, September 25, 1957.

20. Fritz Sternberg, The Coming Crisis (third Impression; John Day Co. Inc., New York, 1947), p.97.

21. J.A. Hobson, The Evolution of Modern Capitalism (Charles Scribner’s Sons, New York, 1916), p.460.

22. A major attempt at secular analysis was made by the Russian economist Kondratieff in the early twenties. He attempted, however, to link production and prices in a series of 50-year repetitive cycles, with the cycles unrelated as to upward or downward direction. His methodology was criticized by Trotsky as well as by Russian specialists in economics. The consensus seems to be that no statistical basis exists for his cycles, at least so far as production is concerned. However, some bourgeois economists have tended to recognize them or to seek them, at any rate, in terms of price series alone. Schumpeter has attempted to use these Kondratieffs, but primarily in relation to his theory on the role of innovators in capitalist progress. Kondratieff himself was exiled to Siberia in 1930 as the alleged head of a “subversive” Workers and Peasants party.

23. Florence Peterson, Survey of Labor Economics (Harper & Brothers, New York, 1947), pp.418-21.

24. Moulton, Income and Economic Progress, op. cit., pp.181-2.

25. Harold Faulkner, American Economic History (fifth edition; Harper & Brothers, New York, 1943), p.404.

26. I am paraphrasing Maurice Dobb’s succinct statement on the decisive ratios in his review of The Theory of Capitalist Development by Paul Sweezy. He is critical of Sweezy’s undercon-sumptionist approach. Science and Society, Summer 1943, p.273.

27. Kuznets, op. cit., p.51.

28. Capital (Everyman’s Library; E. p.Button & Co. Inc., New York, 1932), I, 484.

29. Thomas Ellison, The Cotton Trade of Great Britain, as quoted by Kuznets, op. cit., p.14.

30. Louis Hacker, The Triumph of American Capitalism (Simon & Schuster, New York, 1940), p.418,

31. Kuznets, op. cit., p.49.

32. Karl Marx, Value, Price and Profit (edited by Eleanor Marx Aveling; International Publishers, New York), pp.16-19.

33. Moulton, Controlling Factors In Economic Development, op. cit., p.282.

Main ISR Index | Main Newspaper Index

Encyclopedia of Trotskyism | Marxists’ Internet Archive

Last updated on: 30 April 2009